Navigating Condo Project Reviews for Lenders

Condo project reviews have always been an issue for lenders. The problem is that condo reviews do not really fit into the loan underwriting cycle. The review is only needed for a fraction of properties (about 7-8 per 100 transactions), which means there is no standardized process for dealing with them.

The Issue with Condo Project Reviews

Most underwriters are well-trained to do credit reviews. Because of the lower volume of condo loans in the pipeline, underwriters find condo project reviews are much harder to complete than credit reviews.

Fannie and Freddie do not make it easier, either. There are multiple layers of guidelines and additional checks that need to be completed for each project review to ensure that Fannie/Freddie will then agree to buy the mortgage.

The process is confusing and very time-consuming – you have to check the guidelines, the questionnaire, and the documents from the associations, none of which is pleasant or easy, while at the same time, the stakes are high since one simple mistake can be really costly. At the end of the day, you end up being overworked and drowned in paperwork.

To address this, some larger lenders, like Wells Fargo, have dedicated teams of underwriters dealing with condo project reviews. However, putting together a team of experts is a complex process that requires a lot of time and resources for training.

As there aren’t that many condo loan experts, retaining qualified and well-trained employees becomes a challenging priority for these firms. We also have to take into account market fluctuations and, consequently, the need to downsize or expand the team on short notice. All of this makes the idea of partnering with an expert in the field so much more appealing.

Smaller companies also prefer to entrust this task to a reliable partner who knows how to acquire HOA Documents quickly and how to summarize and analyze them. As they are often pressured by time and the need to provide a highly competitive customer experience, smaller lenders prefer to partner with a condo project review expert to finalize the review process quickly.

To get a loan approved, you need to collect many documents from different sources. Most documents for credit review are submitted by the borrower or gathered by the realtor. Then there are the credit reports, employment verifications, etc., which can usually be obtained with a click of a button.

However, the condo project review is unique and requires the lender to follow a convoluted, time-consuming, and error-prone process of reaching out to condos or builders to obtain the necessary documents.

If a condo is missed altogether, or you get late or incorrect information, you will face several potential consequences:

- Miscalculating the borrowing potential – the condo fees might be too high for the buyer.

- Lost revenue. Incorrect Fannie/Freddie eligibility analysis might lead to not being able to sell the mortgage to Fannie or Freddie. This would mean turning to a secondary market, which in most cases means loss of revenue.

This is why you need to make sure you obtain all the right documents on time and never miss anything in the review. HOAs and condo associations are famous for their slow responses and hundreds of pages of scanned and difficult-to-read legal documents, so many lenders use a feasible solution of turning to someone who deals with HOAs on a daily basis, like us.

The Complexity and Requirements of a Condo Project Review

Lenders usually have Fannie-specified guidelines to follow when working on condo projects. Sometimes a lender would also have their own investor requirements depending on who they are selling the loans to. This means having a tailored questionnaire with more specific questions to fill in, which delays the process even further.

What happens when you make a mistake in the review? You can’t sell the loan, and it stays in your books. Or you sell it on the secondary market and lose money. This is why you really need to pay attention to the requirements.

The hard part with Fannie’s and Freddie’s requirements for condo project reviews is getting all the right information with the right context for every question. The HOA documents are lengthy and convoluted, which increases the chances of incorrectly calculating the commercial space, identifying the subject property phase, etc.

Lenders often use legal language that is different from that of the HOAs. Because of that, HOAs can sometimes interpret the question incorrectly, and the underwriter needs to identify that mistake and get it corrected before sending the review. One missed or misunderstood question would mean an illegible project.

There isn’t a particular question that requires more attention, and everything needs to be carefully scrutinized. But here is a comprehensive list of the most critical items that would make a project ineligible:

| Ineligible Project Characteristics | Condo Project Type | Co-op Project Type |

|---|---|---|

| Timeshare, fractional, or segmented ownership projects. | ✔ | ✔ |

| New projects where the seller is offering sale or financing structures in excess of Fannie Mae’s eligibility policies for individual mortgage loans. These excessive structures include but are not limited to, builder/developer contributions, sales concessions, HOA assessments, principal and interest payment abatements, and/or contributions not disclosed on the settlement statement. | ✔ | ✔ |

| Any project that permits a priority lien for unpaid common expenses in excess of Fannie Mae’s priority lien limitations. | ✔ | |

| Co-op projects that are subject to leasehold estates. | ✔ | |

| Limited or shared equity co-ops that have not been approved by Fannie Mae through the PERS process, as required. These are projects in which the co-op corporation places a limit on the amount of return that can be received when stock or shares are sold. | ✔ | |

| A tax-sheltered syndicate’s leasing to a co-op or “leasing” co-ops – projects that involve the leasing of the land and the improvements to the co-op corporation, even if the co-op corporation owns part of the building. | ✔ | |

| Co-op projects in which the developer or sponsor has an ownership interest or other rights in the project real estate or facilities other than the interest or rights it has in relation to unsold units. | ✔ | |

| Projects that are managed and operated as a hotel or motel, even though the units are individually owned. | ✔ | ✔ |

| Projects with covenants, conditions, and restrictions that split ownership of the property or curtail an individual borrower’s ability to utilize the property. | ✔ | ✔ |

| Multi-dwelling unit projects that permit an owner to hold title (or stock ownership and the accompanying occupancy rights) to more than one dwelling unit, with ownership of all of his or her owned units (or shares) evidenced by a single deed and financed by a single mortgage (or share loan). | ✔ | ✔ |

| Projects with property that is not real estate, such as houseboat projects. | ✔ | ✔ |

| Any project that is owned or operated as a continuing care facility. | ✔ | ✔ |

| Projects with non-incidental business operations owned or operated by the HOA include but are not limited to, a restaurant, spa, or health club. | ✔ | |

| The total space that is used for non-residential or commercial purposes may not exceed 35%. | ✔ | ✔ |

| Projects with mandatory upfront or periodic membership fees for the use of recreational amenities, such as country club facilities and golf courses, are owned by an outside party (including the developer or builder). Membership fees paid for the use of recreational amenities owned exclusively by the HOA or master association are acceptable. | ✔ | ✔ |

| Projects that do not meet the requirements for live-work projects. | ✔ | ✔ |

| Projects in which the HOA or co-op corporation is named as a party to pending litigation or for which the project sponsor or developer is named as a party to pending litigation that relates to the safety, structural soundness, habitability, or functional use of the project. | ✔ | ✔ |

| Projects in which a single entity (the same individual, investor group, partnership, or corporation) owns more than the following total number of units in the project: projects with 5 to 20 units – 2 projects with 21 or more units – 20% | ✔ | ✔ |

For more information on this, check Fannie Mae.

Making condo project reviews easy

We are here to help, and this is how.

After we identify the HOA, we send them the questionnaire link or the pdf file to fill in, depending on their preferences.

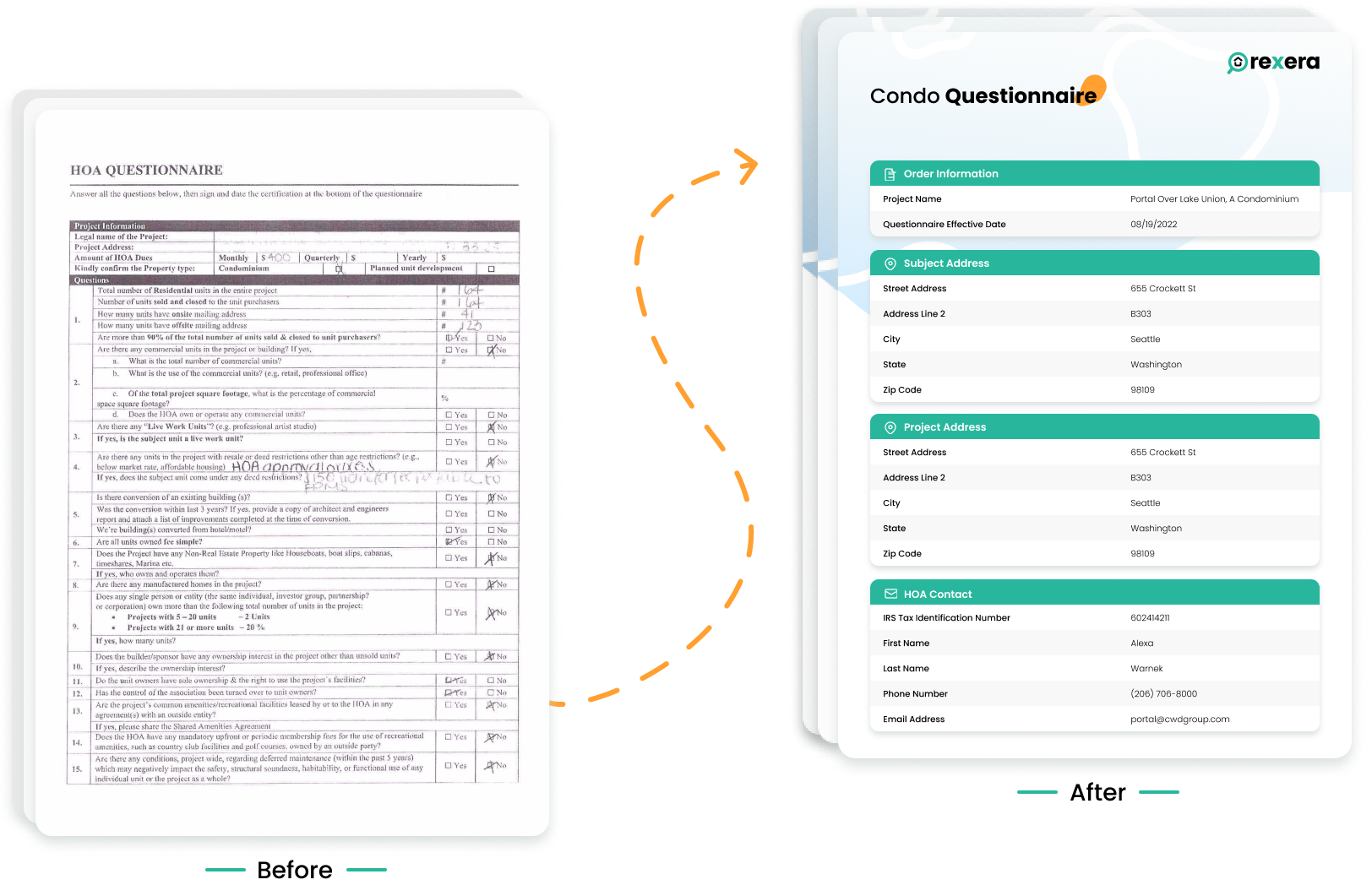

Sometimes the HOA documents are handwritten, which often presents challenges for underwriters. That’s why our Engineering team built an algorithm that analyzes handwritten documents and turns them into easily readable PDFs like this:

Once we receive the completed set of questions, our algorithms will run the answers through the built-in logic to create an approval report. For certain complex questions related to insurance, budgets, CC&R, and similar, our analysts would review the answers manually and mark them in the system as completed.

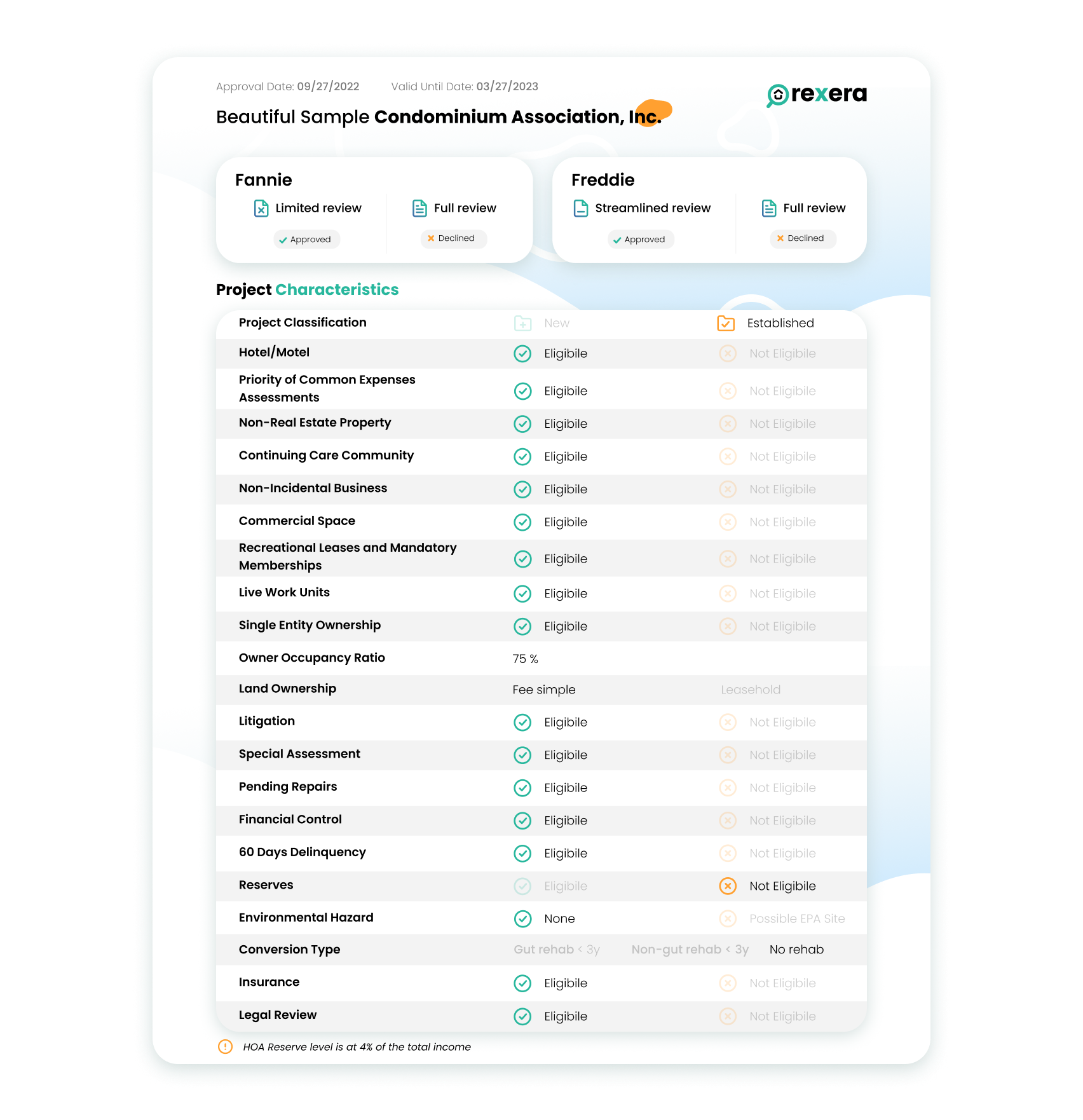

Once all answers, both checked by the algorithm and reviewed by our analysts, are ready, our system will generate an eligibility report, which highlights whether a project is eligible for a full review or a limited review and whether it is eligible for Fannie or Freddie.

We usually do a full review for all condo project reviews so that in case the loan does not qualify for the limited review, the lender can use the full review and utilize the same approval without the need to go over the documents again. The lender will also know from the project review perspective whether they can increase or decrease the LTV.

Because everyone has different needs, we offer Condo Project Document Acquisition and Condo Project Review as separate offerings or as a bundle, in case you don’t have time to deal with the paperwork. Reach out to us for more info.

We also share Real Estate insights on LinkedIn! Follow our page to stay up-to-date with the news

Suggested Posts

Rexera in the News

This is a huge win for us – so THANK YOU for all you do!"